Business travel bottoms out, near-term optimism remains high

(Pandemic travel sentiment 2 of 2)

As we have watched travel come to a near standstill due to the COVID-19 pandemic, questions and opinions abound on how its affect will vary across different segments or categories. Will corporate or leisure travel return first? Will travel permanently become a smaller part of how the world does business?

We have some hints as to how the business travel community is viewing the evolving situation, thanks to the Global Business Travel Association, which was quick to begin polling its membership on the crisis. It fielded its first coronavirus-related survey February 4, before the disease even had an official name. There are many things I wish were different about the series and how GBTA shares it (see comments at the end of this post), but their quickness to take their members’ pulse has allowed them to track sentiment over time.

My biggest takeaways from watching the GBTA poll results up through the latest on April 8, are that active business travel has essentially bottomed out, and expectations for its return are probably overly optimistic, despite shifting in a huge way between March 23 and April 8.

Business travel bottoms out

GBTA’s survey results indicate, unsurprisingly, that business travel has bottomed out. The global average percentage of business trips for March and April that respondents say have been cancelled as a result of the coronavirus is 92% (as of the April 8 poll). What is that 8% of trips that remain? It probably contains a tiny share of trips considered essential for the remainder of April, but given the extent of stay-at-home orders and flight capacity reduction, early March trips probably account for much of it.

It is fair to say, based on that 92%, that the only business trips happening now are those deemed absolutely essential. So if we are at the bottom, how long will we be here?

Recovery timing more realistic, still optimistic

GBTA members’ expectations for travel’s return have shifted significantly from March 23 to April 8. They express more clarity about how long travel will be on pause – 40% said in the earlier survey they were unsure when trips would resume, but two weeks later, that was down to just 16%.

As they have become more confident, respondents are seeing a longer timeline for reduced travel. The most striking shift by far is an increase in respondents who do not see regular business travel returning for a year or more. On March 23, just 1% of respondents said they expected a 12-month wait, and just two weeks later, 28% said that do not see regular business travel coming back for longer than 12 months. The April 8 version of GBTA’s poll shows more than half of respondents expect regular business travel to resume within two to three months, which I find overly optimistic.

It is important to note that the question specifies “regular” business travel, so it’s not the case that more than a quarter of respondents expect NO business travel until early 2021. It would be interesting to see GBTA take the survey further as the future becomes a little clearer. When will domestic trips resume? International? Will the length of flight, number of connections, and regions visited be taken into account in a new way? And what about conferences? Many have already been cancelled and postponed. With so many now scheduled to take place in the last 4-5 months of the year, attendance will suffer even in the best scenario. And will meetings and conferences be generally shunned or limited until after a vaccine is developed?

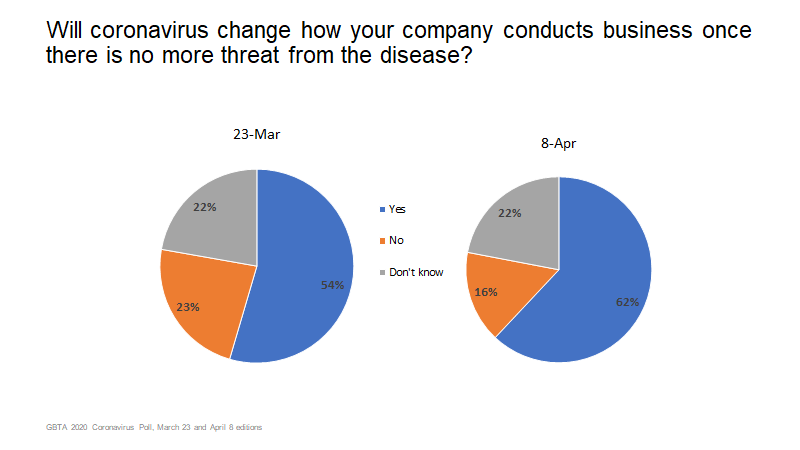

Will travel become a smaller part of doing business?

A theory that I have heard here and there over the past few weeks: All these Zoom meetings have been so productive, even when the health crisis has passed and the global economy is fully recovered, business travel will never come back in a big way. The closest that the GBTA survey comes to addressing this is the below question:

Unfortunately, that doesn’t help assess the future of business travel in light of this situation. The question is too vague and the survey includes too many different kinds of stakeholders. I would love to see GBTA add more specific questions, like: “When the COVID19 health crisis has passed, and the global economy is in recovery mode, how do you expect travel’s role in your business operations to compare to its role in 2019?” I would also love to see specific questions about their plans to reconnect with clients after the crisis abates, and how they feel virtual meetings – internally, for sales initiatives, and externally for project execution – compare to face-to-face.

Methodology Musings: Shortcomings of the GBTA data

Again, I commend GBTA for their quickness to begin taking members’ pulse. They began fielding February 4, the earliest I am aware of any American travel organization launching a coronavirus survey. No travel research company even moved that quickly. But below are some of the caveats to keep in mind when looking at the GBTA survey results:

· The questions have changed from survey to survey. I actually applaud this – surveys that insist on sticking to questions simply to enable comparison over time can quickly become irrelevant. Still, it is important to keep in mind that it is hard to compare the February 4 results with the April 8 results.

· All geographic regions are mixed into one pool. GBTA is based in the U.S., and leadership positions are held primarily by Americans, so I assume the biggest share of respondents is US-based. Still, it would be nice to see results by region.

· All types of company are mixed into one pool. GBTA is transparent about who responds, and typically about half of their respondents are travel managers/buyers and procurement professionals. It would be useful to see the responses of just these two groups, and to launch a different survey for suppliers and TMCs.

With business travel essentially bottomed out, it would be great to see GBTA start asking some more probing questions about how companies will decide to resume travel, and the extent to which wider adoption of video conferencing will or will not decrease business travel in a post-COVID19 world.